Horne, a raisin farmer, has been breaking the law for 11 solid years. He now owes the U.S. government at least $650,000 in unpaid fines. And 1.2 million pounds of unpaid raisins, roughly equal to his entire harvest for four years.

His crime? Horne defied one of the strangest arms of the federal bureaucracy — a farm program created to solve a problem during the Truman administration, and never turned off. […]

It works like this: In a given year, the government may decide that farmers are growing more raisins than Americans will want to eat. That would cause supply to outstrip demand. Raisin prices would drop. And raisin farmers might go out of business.

To prevent that, the government does something drastic. It takes away a percentage of every farmer’s raisins. Often, without paying for them.

These seized raisins are put into a government-controlled “reserve” and kept off U.S. markets.

When she became pregnant, Ms. Martin called her local hospital inquiring about the price of maternity care; the finance office at first said it did not know, and then gave her a range of $4,000 to $45,000. […]

Like Ms. Martin, plenty of other pregnant women are getting sticker shock in the United States, where charges for delivery have about tripled since 1996, according to an analysis done for The New York Times by Truven Health Analytics. Childbirth in the United States is uniquely expensive, and maternity and newborn care constitute the single biggest category of hospital payouts for most commercial insurers and state Medicaid programs. […]

The average total price charged for pregnancy and newborn care was about $30,000 for a vaginal delivery and $50,000 for a C-section, with commercial insurers paying out an average of $18,329 and $27,866, the report found. […]

Two decades ago, women typically paid nothing other than a small fee if they opted for a private hospital room or television.

Another power law […] is Benford’s Law, which states that the distribution of digits in a lot of data are not even, but power law distributed. For example, in base 10, the number one should, all things being equal, appear 10% of the time. But in many data sources one appears around 30% of the time. This fact is actually used to help detect fraud in, for example, tax returns.

Wells Fargo & Co., the largest U.S. mortgage lender, is offering 30-year fixed-rate loans at 4.5 percent, according to its website, up from 4.13 percent on June 18 and 3.88 percent on May 22, when comments by Bernanke to lawmakers and the release of the minutes of the last Fed meeting caused bonds to plummet.

So in one month, the average 30 year fixed rate mortgage has jumped by over 60 basis points. What does this mean for net purchasing power? […] Assuming a $2000/month budget to be spent on amortizing a mortgage (or otherwise spent for rent), it means that suddenly instead of being able to afford a $425K house, the average consumer can buy a $395K house.

This means that, all else equal, housing just sustained a 7% drop in the average equlibrium price based on what buyers can afford.

{ When every talking head is bullish and the world is going so great that we should all “buy stocks,” Santelli demands we ask Bernanke - “what are you afraid of,” that keeps you pumping this much money into the system for this long? | Zero Hedge }

Tim Cook […] reminded a Senate subcommittee that Apple is investing $100 million to make some of its Macintosh computers in the U.S. […] The operation, to be based in Texas, will be Apple’s first domestic assembly foray since 2004, and other technology manufacturers are moving jobs onshore. Google Inc.’s Motorola Mobility, for example, also plans to assemble smartphones in Texas.

It’s not all public relations: These companies are taking advantage of low energy costs and a decade of wage stagnation, which has made U.S. factory jobs more competitive with those in China, where wages are rising.

Back in 1996, economist Paul Krugman wrote an essay about the next 100 years of economic history, as if looking back from the year 2096. […]

When something becomes abundant, it also becomes cheap. A world awash in information is one in which information has very little market value. In general, when the economy becomes extremely good at doing something, that activity becomes less, rather than more, important. Late-20th-century America was supremely efficient at growing food; that was why it had hardly any farmers. Late-21st-century America is supremely efficient at processing routine information; that is why traditional white-collar workers have virtually disappeared.

… Many of the jobs that once required a college degree have been eliminated. The others can be done by any intelligent person, whether or not she has studied world literature.

REITs [Real Estate Investment Trust] are sold like stocks, and they’re held by many individuals and institutional investors. You might have a REIT in your retirement fund. REITs are trusts that own and develop property and earn rental income. […] “They are forced by law — a law created in 1960 — that provides that real estate investment trusts have to meet certain tests,” says Brad Thomas, editor of the Intelligent REIT Investor. “And if they do, they are forced to pay out 90 percent of their taxable income in the form of dividends.” Those dividends are a regular stream of income, and they’re what make REITs attractive to investors.

I put down $513.94 on a REIT index fund. It’s basically a smorgasbord of many different REITs. It contains what you might expect — REITs that own apartment buildings and shopping centers. But Thomas says the range of REITs today goes far beyond that, “from billboards to prisons to cell towers, campus housing. Even solar is on the horizon potentially.”

The US Supreme Court today ruled that Myriad, the US biotech company that holds a monopoly on testing for a set of breast-cancer related genes, can’t hold a patent on genetic material. But after the news broke, Myriad’s stock shot up.

Here’s why: […] While the court ruled that a gene in its natural state is something that can’t be owned—even if it’s been isolated, which Myriad argued warranted a patent—it also ruled that complementary DNA, or cDNA, could be proprietary. Created artificially in the lab, the cDNA version of the BRCA genes lack so-called “junk” DNA, the pieces that don’t contribute to the gene’s production of proteins. This technical difference, according to the ruling, makes the genes unique enough to be distinguished legally from their natural cousins.

There are somewhere between 50 million and 100 million farms in the world (if you exclude those smaller than about three American football fields). But about half the crops produced by those farms rely on the seeds, fertilizers, and pesticides supplied by a mere dozen or so companies. Most of those crops are bought, traded, and transported around the world by another half dozen. […] And when it’s time for agricultural products to be processed and distributed to stores, that’s another dozen or so, many overlapping with the aforementioned traders and suppliers. […]

Researchers and activists have questioned the safety or long-term consequences (or both) of various Big Ag [Big Agriculture] practices, such as the use of certain pesticides, fertilizers, animal hormones, and food additives. […] Among the other specific complaints these days are deforestation and negligence. In Brazil, for example, a tripling of soybean production since 1990 has been blamed for the ongoing stripping of the Amazon basin. In the United States, ill-managed factory farms and processing plants have contributed to repeated outbreaks of food-borne illnesses that kill about a thousand people a year and sicken millions. […]

For farmers, oligopolies mean fewer choices of supplier and sometimes no choice at all about whom they will sell to. One ongoing trend is contract farming, in which farmers grow according to a food company’s specifications, with all supplies provided by the company, in return for its commitment to purchase the farmers’ output if it is acceptable.

U.S. stocks fell on Wednesday, with the Dow sliding more than 100 points.

The Dow is now riding a three-day losing skid, capped by today’s 126-point drop, marking the first time this year the blue-chip average has suffered three straight down days.

With it all said and done, the Dow went 112 trading days without a three-day losing streak, the longest such stretch in its history. The previous record was set in 1935, when the Dow went 93 trading days without three straight down days.

I read two or three business plans a week. I’ve developed a checklist of irritating elements that entrepreneurs are best advised to avoid if they want to succeed in raising finance.

Complicated and aggressive non-disclosure and confidentiality agreements

There is often an inverse relationship between the length of the NDA and the scale of the project. While entrepreneurs should try to protect their intellectual property, these contracts are really more of a ritual than of any practical use.

Advisers taking a disproportionate fee

I was presented with a plan last year where the adviser stood to collect 20 per cent of the funds raised. It put me off the proposition. […]

Founders offering no “hurt money”

I want to see the promoters having plenty on the line, to make sure they don’t give up too easily if the scheme goes wrong. […]

Complex financial modelling

I read a plan recently for a £100,000 revenue confectionery business that had 10 tabs of Excel spreadsheets. My eyes swam when I tried to understand it. […]

Too much focus on five-year financial projections

What interests me are the next 12 to 18 months – further out is pure speculation, especially for an early-stage business. I never buy shares based on what might be possible years away – I want to see what milestones can be achieved in the near future.

The airwaves are full of stories of economic recovery. One trumpeted recently has been the rapid recovery in housing, at least as measured in prices.

The problem is, a good portion of the rebound in house prices in many markets has less to do with renewed optimism, new jobs, and rising wages, and more to do with big money investors fueled by the ultra-cheap money policies of the Fed.

On my recent trip to Salt Lake City, Utah, after presenting to a bi-partisan audience in the Capitol building, a gentleman came up to me and introduced himself as a real estate agent. He explained that he’d been seeing something very strange over the past six months, where very well capitalized, out-of-state private equity funds had been buying up huge swaths of residential real estate with cash.

The effect, not surprisingly, is that regular home buyers are being outbid and eventually priced out of the market. Over time, these full cash offers at the ask get noticed and home sellers begin to raise their asking prices.

[W]e were surprised to see an article in the very much mainstream, and pro-administration policies NYT, exposing just this facet of the new housing bubble. […]

Blackstone, which helped define a period of Wall Street hyperwealth, has bought some 26,000 homes in nine states. Colony Capital, a Los Angeles-based investment firm, is spending $250 million each month and already owns 10,000 properties. With little fanfare, these and other financial companies have become significant landlords on Main Street. Most of the firms are renting out the homes, with the possibility of unloading them at a profit when prices rise far enough.

Processed-food companies increasingly turn to their legions of scientists to produce foods that we can’t resist. These food geeks tweak their products by varying the levels of the three so-called pillar ingredients—salt, sugar, and fat. […]

[The] optimum amount of salt, sugar, or fat is called the bliss point. Scientists also adjust these ingredients as well as factors such as crunchiness to produce a mouthfeel—that is, the way the food feels inside a person’s mouth—that causes consumers to crave more. Technologists can also induce a flavor burst by altering the size and shape of the salt crystals themselves so that they basically assault the taste buds into submission.

The holy grail of junk-food science is vanishing caloric density, where the food melts in your mouth so quickly that the brain is fooled into thinking it’s hardly consuming any calories at all, so it just keeps snacking.

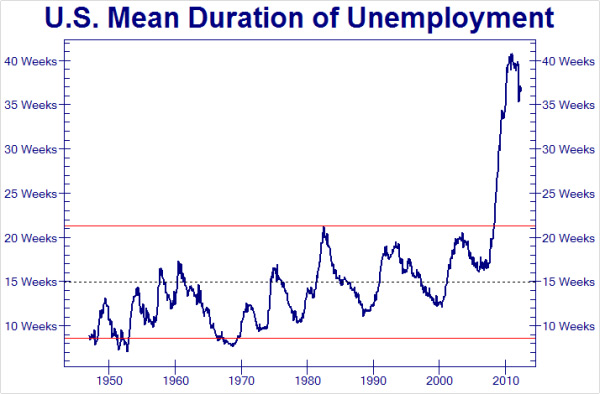

American households have rebuilt less than half of the wealth lost during the recession, according to a new analysis from the Federal Reserve, hampering the country’s economic recovery.

The research from the St. Louis Fed shows that households had accumulated net worth totaling $66 trillion at the end of last year. After adjusting for inflation and population growth, the bank found that meant families on average have only made up 45 percent of the decline in their net worth since the peak of the boom in 2007.

In addition, most of the improvement was due to gains in the stock market, according to the report, primarily benefiting wealthy families. That means the recovery for most households was even weaker. […]

The Fed is spending $85 billion a month to lower long-term interest rates and stimulate the economy. It has also kept short-term interest rates to near zero. That has helped push stock markets to record highs, while home prices have jumped by the most in seven years. Consumer confidence is at its highest point since February 2008. Officials hope those factors will eventually result in more consumer spending power.

Uncertainty exists about how markets will reestablish normal valuations when the Fed withdraws from the market. It will likely be difficult to unwind policy accommodation, and the end of monetary easing may be painful for consumers and businesses. Given the Fed’s balance sheet increase of approximately $2.5 trillion since 2008, the Fed may now be perceived as integral to the housing finance system.

Yahoo didn’t just buy a company, it validated, to the tune of a billion dollars, the notion that bad business is worth pursuing. The entire concept of what makes something a good idea continues to be inverted, warped, and thrown in a gully. This is the idea economy, remember—the industry of fantasy. It doesn’t have to “make sense.” Money isn’t valuable. Success isn’t lucrative. Profit is pointless. These are the industry’s norms. All you need to do to become a billion-dollar business is make people entertained and vaguely interested.

David Karp did just that. Over 100 million entranced humans blog with Tumblr, and not a single one pays for the privilege. They’re free to swap reality show GIFs, aspirational shopping photos, and masturbate, with only the faintest whisper of marketing reaching their ears.

Edward Glaeser: If you look back 120 years ago or so, Detroit looked like one of the most entrepreneurial places on the planet. It seemed as if there was an automotive genius on every street corner. If you look back 60 years ago, Detroit was among the most productive places on the planet, with the companies that were formed by those automotive geniuses coming to fruition and producing cars that were the technological wonder of the world. So, Detroit’s decline is of more recent heritage, of the past 50 years. […] And it tells us a great deal about the way that cities work and the way that local economies function. […] If we go back to those small-scale entrepreneurs of 120 years ago–it’s not just Henry Ford; it’s the Dodge brothers, the Fisher brothers, David Dunbar Buick, Billy Durant nearby Flint–all of these men were trying to figure out how to solve this technological problem, making the automobile cost effective, produce cheap, solid cars for ordinary people to run in the world. They managed to do that, Ford above all, by taking advantage of each other’s ideas, each other supplies, financing that was collaboratively arranged. And together they were able to achieve this remarkable technological feat. The problem was the big idea was a vast, vertically integrated factory. And that’s a great recipe for short run productivity, but a really bad recipe for long run reinvention. And a bad recipe for urban areas more generally, because once you’ve got a River Rouge plant, once you’ve got this mass vertically integrated factory, it doesn’t need the city; it doesn’t give to the city. It’s very, very productive but you could move it outside the city, as indeed Ford did when he moved his plant from the central city of Detroit to River Rouge. And then of course once you are at this stage of the technology of an industry, you can move those plants to wherever it is that cost minimization dictates you should go. And that’s of course exactly what happens. Jobs first suburbanized, then moved to lower cost areas. The work of Tom Holmes at the U. of Minnesota shows how remarkable the difference is in state policies towards unions, labor, how powerful those policies were in explaining industrial growth after 1947. And of course it globalizes. It leaves cities altogether. […] It was precisely because Detroit had these incredibly productive machines that they squeezed out all other sources of invention–rather than having lots of small entrepreneurs you had middle managers for General Motors (GM) and Ford. […]

Russ Roberts: So, one way to describe what you are saying is in the early part of the 20th century, Detroit was something like Silicon Valley, a hub of creative talent, a lot of complementarity between the ideas and the supply chain and interactions between those people that all came together. Lots of competition, which encouraged people to try harder and innovate, or do the best they could. Are you suggesting then that Silicon Valley is prone to this kind of change at some point? If the computer were to become less important somewhere down the road or produced in a different way?

Edward Glaeser: The question is to what extent do the Silicon Valley firms become dominated by very strong returns to scale, a few dominant firms capitalize on it. I think it’s built into the genes of every industry that they will eventually decline. The question is whether or not the region then reinvents itself. And there are two things that enable particular regions to reinvent themselves. One is skills, measured education, human capital. The year, the share or the fraction in the metropolitan area with a college degree as of 1940 or 1960 or 1970 has been a very good predictor of whether, particularly northeastern or northwestern metropolitan areas, have been able to turn themselves around. And a particular form of human capital, entrepreneurial human capital, also seems to be critical, despite the fact that our proxies for entrepreneurial talent are relatively weak. We typically use things like the number of establishments per worker in a given area, or the share of employment in startups from some initial time period. Those weak proxies are still very, very strong predictors of urban regeneration, places that have lots of little firms have managed to do much better than places that were dominated by a few large firms, particularly if they are in a single industry. So, let’s think for a second about Silicon Valley. Silicon Valley has lots of skilled workers. That’s good. But what I don’t know is whether Silicon Valley is going to look like it’s dominated by a few large firms, Google playing the role of General Motors. Or whether or not it will continue to have lots of little startups. There’s nothing wrong with big firms in terms of productivity. But they tend to train middle managers, not entrepreneurs.